Most Indian founders treat fundraising like a numbers game: build a list of 50 VCs, send the same deck to all of them, and wait for someone to say yes. The results are predictable - weeks of silence, a handful of polite rejections, and a creeping suspicion that the startup is the problem.

Usually it is not. The most common cause of fundraising failure in India in 2026 is not a bad startup - it is a mismatched investor. Stage mismatch, sector mismatch, cheque size mismatch, thesis mismatch (which we covered in detail in What Is a VC Investment Thesis?). Any one of these will kill a conversation before it starts, no matter how good the product is.

This guide gives you a concrete, step-by-step system for finding the right VC for your specific startup - not a generic list of investors, but a personalised shortlist of 10 to 15 funds who are structurally likely to say yes to what you are building. We also cover how to approach them, what the most common mistakes look like, and what to do when you get a no.

Why most Indian founders approach the wrong VCs

Before the step-by-step, it helps to understand the failure modes. Based on patterns from India's 2025 fundraising landscape, here are the five most common reasons founders end up pitching the wrong investors:

- They pitch by brand, not by fit: Sequoia (now Peak XV), Accel, and Lightspeed are household names. They are also multi-stage funds that primarily write Series A cheques of $5M+. A pre-revenue founder with a prototype pitching Peak XV is not being ambitious - they are wasting a contact and burning a relationship that could have been useful two years from now. (Instead, refer to our list of Top 20 VC Firms in India).

- They confuse 'investing in tech' with 'investing in my sector': A fund that has backed fintech, SaaS, and consumer apps is not necessarily a fit for your B2B supply chain startup. Sector labels are shallow. What matters is the specific subsector, business model, and customer segment each fund has conviction in - and that only becomes clear when you read their portfolio, not their website.

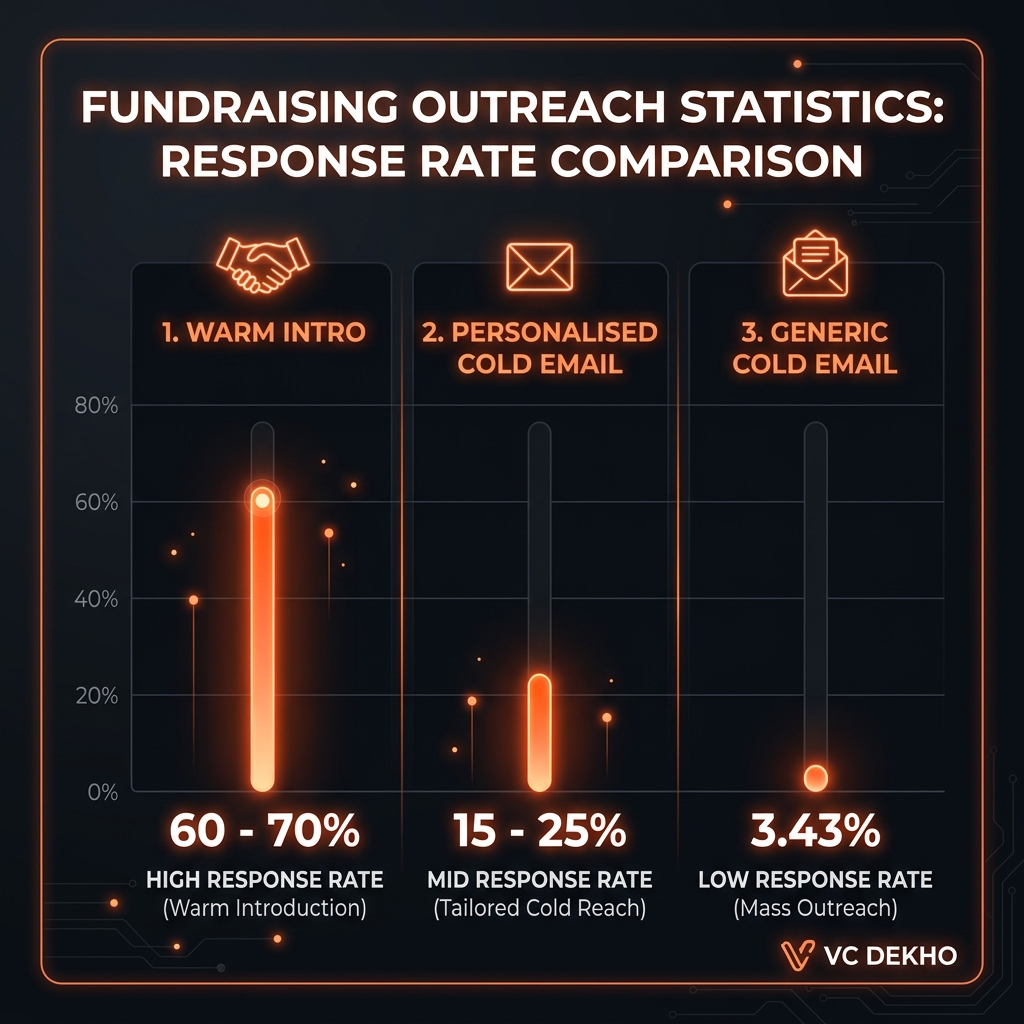

- They send the same cold email to everyone: The average cold email reply rate from VCs dropped to 3.43% in 2026. The top 10% of founders still hit 15–25% - because they send personalised, thesis-specific outreach to a short, well-researched list. Generic mass emails are not just ineffective; they actively signal to the investor that you have not done your homework.

- They fundraise too late: Starting a fundraise when you have two months of runway is not fundraising - it is desperation. Indian VCs can tell the difference, and they price it in. A seed round in India in 2026 takes 3 to 6 months from first meeting to money in the bank. Start your process with at least 8 to 10 months of runway remaining.

- They pitch to investors who have already deployed their fund: A fund that closed a $50M vehicle two years ago and has made 20 investments has very little dry powder left. Researching whether a fund is actively deploying capital - not just whether they exist - is a basic step that most founders skip.

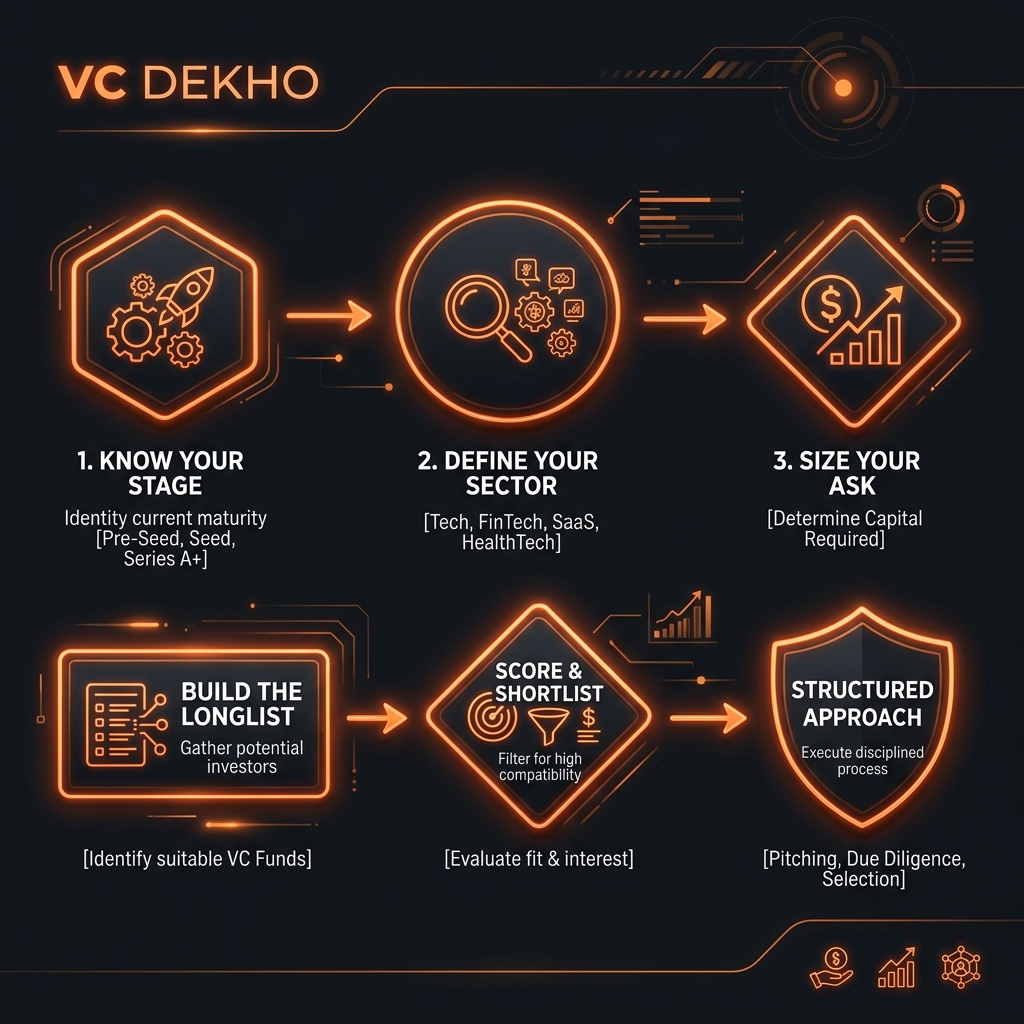

The 6-step framework for finding your right VC

This framework is designed to take you from a blank shortlist to a high-conviction list of 10 to 15 investors in under one week of focused research.

STEP 1: Be honest about your stage

FoundationBefore you open a browser, answer one question honestly: what stage is your startup actually at right now - not where you hope to be in six months?

- Pre-seed: Idea or prototype, little to no revenue, no product-market fit signal yet. You need a micro VC or angel (see the Best Micro VCs India writing the first cheque).

- Seed: Early product in market, first paying customers or strong user traction, beginning to understand what drives retention. You need a seed fund or early-stage VC.

- Series A: Proven model, $1M+ ARR or equivalent engagement metrics, clear unit economics, ready to scale a repeatable go-to-market. You need a multi-stage or growth fund.

The rule: only target funds whose primary stage matches yours. A fund that 'also does pre-seed sometimes' is not a pre-seed fund. Do not pitch them for your first round. (For a deep dive on stages, check our guide on Pre-Seed vs Seed vs Series A).

STEP 2: Define your sector at the subsector level

AlignmentSector fit is not about the broad label - it is about the specific problem and business model within that sector.

- Bad definition: "We are a fintech startup."

- Good definition: "We are a B2B lending infrastructure play targeting NBFCs and co-lending models."

The difference matters because a fund that backs consumer fintech apps has completely different conviction, portfolio, and networks than one that backs fintech infrastructure. They are not interchangeable.

Write your subsector definition in one sentence before you begin your research. Use it as a filter for every fund you evaluate: does this fund have at least two portfolio companies that sit in the same subsector or business model?

STEP 3: Size your ask to the right fund tier

EconomicsFund size determines cheque size. This is arithmetic, not opinion. A $25M micro VC cannot write a $3M cheque - it would be 12% of their entire fund in one deal. A $500M multi-stage fund will not write a $300K cheque - it moves the needle on their returns by exactly nothing.

The rule of thumb: a fund's initial cheque is typically 2–5% of their total corpus.

- If you are raising ₹2 crore ($250K): target funds with corpus of $5M–$15M.

- If you are raising ₹4 crore to ₹16 crore ($500K–$2M): target funds with corpus of $15M–$60M.

- If you are raising $2M–$5M: target funds with corpus of $50M–$200M.

- If you are raising $5M+: target funds with corpus of $150M+.

Mismatching this is the single most avoidable mistake in Indian fundraising.

STEP 4: Build your longlist using 4 sources

SourcingWith your stage, subsector, and ask defined, you can now build a raw longlist of 30 to 50 investors. Use these four sources:

- Portfolio reverse-engineering: Find 3 to 5 startups in your exact subsector that raised their last round 12–24 months ago. Look at their investors on Crunchbase or Tracxn. Every fund that backed them is a potential fit for you.

- VC blogs and landscape reports: Blume Ventures' micro VC landscape report (April 2026), the Backrr early-stage VC database, and Tracxn's India VC filters are the three most current sources for active Indian funds.

- Founder communities: Soonicorn Club, LetsVenture's founder network, and the comment sections of popular Indian VC partner posts on LinkedIn surface funds that rarely appear in published lists.

- VC Dekho: Join the waitlist at vcdekho.com - our platform is being built specifically to make this research faster and more precise for Indian founders.

STEP 5: Score and shortlist to 10–15 funds

FilteringTake your longlist of 30 to 50 and score each fund on four criteria, 1 to 3:

- Stage fit: (1 = possible stretch, 2 = within range, 3 = exact match)

- Sector fit: (1 = adjacent, 2 = related portfolio, 3 = directly in subsector)

- Cheque fit: (1 = edge of range, 2 = within range, 3 = centre of range)

- Active deployment: (1 = unclear, 2 = probably active, 3 = confirmed recent deal)

Only funds scoring 10 or above out of 12 go on your shortlist.

This sounds harsh - it is meant to be. A shortlist of 12 high-conviction funds will outperform a spray of 50 average-fit funds every single time. For each shortlisted fund, note: the specific partner to approach (not just the fund name), one portfolio company in common with your subsector, and one recent public statement or post from that partner that signals thesis alignment.

STEP 6: Approach in the right order and method

ExecutionNow you are ready to reach out. The order matters:

- Week 1–2: Warm intros first. Map your shortlist to your existing network - advisors, angels, accelerator alumni, fellow founders who have raised from these funds. A warm intro guarantees at least 5 minutes of attention vs 2 seconds for a cold email. Prioritise the 5 to 6 funds where you have even a second-degree connection.

- Week 3–4: Cold outreach for the remaining funds. Personalised, short, thesis-specific emails to the specific partner - not a general inbox. See the templates below.

- Week 5 onwards: Run parallel conversations. Do not wait for one fund to respond before approaching the next. Competition between investors - even implied - accelerates decisions. If you get a soft yes from one fund, it is entirely appropriate to tell others that you have early investor interest.

How to get a warm introduction to any Indian VC

A warm intro is not a favour - it is a skill you can systematically build. Here is how to engineer warm intros even if you feel like you have no network:

- Map the portfolio, not the fund: Every fund on your shortlist has a portfolio page. Pick three portfolio companies in your sector. Find the founders on LinkedIn. Message them directly - not asking for an intro immediately, but with a genuine question about their experience building in your space. Good founders help other founders. Three to four conversations in, an intro request is natural.

- Use accelerator and community alumni networks: Y Combinator, Antler, Krafton, Surge - any accelerator programme you or your co-founder has attended is a warm intro network. So is BITS Pilani Entrepreneurship Cell, IIT alumni groups, and founder communities like iSPIRT and Soonicorn. These communities exist specifically for this kind of connection.

- Leverage your existing angels: If you have raised from any angel investor - even a small cheque - they are your most powerful intro asset. Angels who have co-invested with a fund, or who know the partners personally, can get you a meeting faster than any other route. Ask every angel you know: "Who on this list do you know well enough to make a genuine intro?"

- Engage with VC content before asking for anything: Follow your target partners on LinkedIn and Twitter/X. Comment meaningfully on their posts - not "great insight!" but actual substantive engagement that demonstrates you understand the space they care about. Do this consistently for 4 to 6 weeks before you send a cold message. By the time you reach out, your name is already familiar.

Cold email templates that actually work for Indian founders

When a warm intro is not possible, a well-crafted cold email can still work - but only if it is short, specific, and thesis-matched. The average cold email reply rate from VCs dropped to 3.43% in 2026. The top founders hit 15–25% because they do three things: address the specific partner by name, reference one specific element of the fund's thesis, and lead with a signal rather than a story.

Here are three templates for different situations:

- Keep every cold email under 150 words. Anything longer signals you cannot prioritise.

- Never attach a PDF deck to a cold email. Link to a password-protected deck on Docsend or Notion if needed.

- Never ask for 'advice' or a 'coffee chat'. Ask for a 20-minute call with a specific agenda.

- Never send from a Gmail address. Use your company domain email.

- One polite follow-up after 7–10 days. If still no reply, move on - do not chase.

7 mistakes Indian founders make when approaching VCs - and how to fix them

What to do when a VC says no

Most founders treat a VC rejection as a dead end. The best founders treat it as a data point and a relationship investment.

- Send a gracious reply within 24 hours. Thank them for their time. No arguing, no pushing back, no asking for detailed feedback in the first message.

- If you have rapport, ask one specific question in a follow-up email: 'Is there one thing about the business that gave you the most pause?' You will not always get an answer, but when you do, it is gold.

- Ask if you can send quarterly updates. Most VCs will say yes. This keeps you in their peripheral vision as you hit milestones that might change their view.

- Add them to your investor update list. A VC who passed in month 3 and receives your month 9 update showing 4x revenue growth often comes back. This happens more than most founders realise.

- Do not burn the relationship by venting frustration publicly or privately. The Indian VC community is small. Partners talk. The founder who handles rejection with grace is remembered - and often referred to another fund.

Realistic fundraising timeline for Indian founders in 2026

One of the most damaging myths in Indian startup fundraising is that a round closes in 4 to 6 weeks. It does not. Here is what a realistic timeline looks like:

| Timeline | Phase | What happens |

|---|---|---|

| Month 1 | Research and shortlisting | Build longlist (30–50 funds) → Score and shortlist (10–15 funds) → Research specific partners → Identify warm intro paths → Prepare deck, data room, and metrics snapshot. |

| Month 2 | First conversations | Send warm intro requests → Begin cold outreach for remaining shortlist → First partner calls → Deck presentations → Initial feedback loop. |

| Month 3–4 | Partner meetings & due diligence | Partner-level meetings → Fund internal discussions → Follow-up data requests → Reference calls from fund to your customers/advisors → Term sheet negotiations begin. |

| Month 5–6 | Legal and closing | Term sheet signed → Legal due diligence → Cap table structuring → SHA and SSA drafting and negotiation → Funds hit bank account. |

Start your fundraise when you have 8–10 months of runway remaining. If you have less than 6 months, you are fundraising from a position of weakness and VCs can tell. Desperation is priced into the term sheet.

Stop guessing. Start matching.

VC Dekho is building India's most complete investor research and matching platform. Search by stage, sector, cheque size, and geography. Read investment thesis. Unlock direct contacts. Close your round faster.

Join the WaitlistFrequently Asked Questions

Start with portfolio reverse-engineering: find 3–5 startups in your exact subsector that raised 12–24 months ago, then look at who invested in them on Crunchbase or Tracxn. Layer in the Blume Ventures micro VC landscape report and the Backrr VC database for active fund lists. VC Dekho is building a platform that makes this research searchable - join the waitlist at vcdekho.com.

Budget 4 to 6 months from first partner meeting to funds in the bank for a seed round. Series A rounds can take 5 to 8 months. Starting your process with 8 to 10 months of runway gives you the time and leverage to run a proper process without desperation pricing.

Warm intros are always better - they guarantee at least 5 minutes of attention versus 2 seconds for a cold email. But well-personalised cold emails to the right partner still work. The top 10% of founders get 15–25% reply rates from cold outreach by keeping emails under 150 words, referencing the fund's specific thesis, and leading with a traction signal.

Quality over quantity. A shortlist of 10 to 15 high-conviction, well-researched funds will outperform a spray of 50 average-fit investors every time. Indian VCs talk to each other. If you are seen as shopping a round widely with low conviction, it damages your positioning with everyone on the list.

Send a gracious reply within 24 hours. Ask one specific follow-up question about what gave them the most pause. Ask if you can send quarterly updates. Add them to your investor update list. Many Indian startup rounds have been closed with a fund that initially passed - the relationship after the 'no' is what makes that possible.

Fundraising is a process, not a lottery

The founders who raise efficiently in India in 2026 are not the ones with the best product or the most impressive background. They are the ones who treat fundraising as a structured process - with research, a scoring system, a sequenced outreach plan, and the patience to run it properly.

The six steps in this guide give you that structure. The research takes about a week. The outreach, managed properly, should run in parallel to your product work - not consume it. And the results, when you match the right investor to the right startup at the right stage, compound faster than any spray-and-pray approach ever will.

For deeper research on every Indian VC's thesis, cheque size, and investment history - in one searchable platform - join the VC Dekho waitlist at vcdekho.com.

Explore related posts

Top 20 VC Firms in India (2026 Guide)

A breakdown of the most active and founder-friendly VC firms in India.

Best Micro VCs in India Writing the First Cheque in 2026

Discover the 15 most active micro VCs in India for early-stage and pre-seed startups.

What Is a VC Investment Thesis? (And Why Founders Should Care)

How to decode what VCs are really looking for before you pitch them.